The phrase secular stagnation was first introduced by Alvin Hansen in a speech he prepared for the AEA meetings in 1938: Economic Progress and Declining Population Growth. If you haven't read the speech, I recommend that you do--it's an interesting and easy read. (Alternatively, Tim Taylor provides a concise and accurate summary here: Secular Stagnation: Back to Alvin Hansen.)

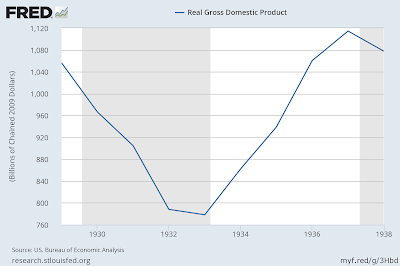

Let's think about what things must have looked like for Hansen in late 1938. Earlier in the decade, the United States suffered a major economic contraction. From 1929-1933, real GDP declined by over 25%. And despite a robust period of growth from 1933-1937, the economy slipped back into recession in 1938.

1938 must have looked disappointing (to say the least) for those living at the time. After a decade of economic hardship (the unemployment rate remained elevated throughout the episode) and recovery, the economy's capacity to produce material wealth in 1938 was no greater than its capacity in 1928. Was this the end of growth?

What sort of growth did Hansen have in mind? Well, writing in 1938, one would probably have been most impressed with the rapid rate of economic expansion that occurred in the late 19th century (the new technologies introduced early in the 20th century would have impressed as well, of course). That was an era of rapid technological progress, high population growth rates, and the widespread development of new territory. Associated with these developments was a rapid growth in investment opportunities and capital spending. Everyone seemed to be working hard. And even if progress was at times interrupted by recession, these episodes were short-lived with rapid recovery. (Personally, I don't think things were quite as rosy as the narrative above suggests, but let's stick to the main story.)

So that's roughly the evidence. What about theory? Hansen notes that earlier economists were focused mainly on how economic growth (driven by technological change, population growth, etc.) affected material living standards (the level of real per capita income). Later economists began to notice that growth and economic stability might be related (the central tenant of modern real business cycle theory). But more recently, Hansen writes, "the role of economic progress in the maintenance of full employment of the productive resources has come under consideration." (It is notable that the economists he cites for initiating this line of inquiry includes Wicksell and not Keynes; see David Laidler).

The theory Hansen espouses seems to relate the level of employment (say, as measured by the employment-to-population ratio or the unemployment rate) to the rate of economic growth. The rate of economic growth is determined by technological progress and population growth. Both of these forces are secular in the sense they tend to operate over extended horizons (i.e., over decades and not from quarter-to-quarter or year-to-year). The effect of growth is to elevate the desire for capital expenditure. A larger population stimulates the construction of residential capital. New industries and technologies stimulate the demand for business fixed investment. Workers are needed to build the stuff. Ergo, a higher rate of growth over long periods of time begets a higher rate of resource utilization over the same period of time (higher average employment rate, lower average unemployment rate).

But the story above is incomplete. After all, what was just described is not inconsistent with (say) real-business-cycle (RBC) theory. The equilibrium level of employment in that class of models could vary with the parameter that describes the economy's long-term growth rate (whether employment is increasing or decreasing in the growth rate is likely to depend on, among other things, the relative strength of substitution and wealth effects). It is theoretically possible to generate secular stagnation in an RBC model, where a low-growth regime generates a low-employment regime. But in the RBC interpretation, low employment could be an efficient outcome, given a lower pace of economic growth. It seems clear that Hansen is suggesting that the low employment observed in a low-growth regime is inefficient. He writes:

For it is an indisputable fact that the prevailing economic system has never been able to reach reasonably full employment or the attainment of its currently realizable real income without making large investment expenditures.

This is a bit of a mischievous statement in that it commingles an alleged fact with theory. (I don't want to make too much of this now, but consider my post here, in particular, the passage by Richard Rogerson related to this issue). Hansen does not get into theory very much at all, except to say:

I shall not attempt any summary statement of this analysis. Nor is this necessary; for I take it that it is accepted by all schools of current economic thought that full employment and the maximum current attainable income level cannot be reached in the modern free enterprise economy without a volume of investment expenditures adequate to fill the gap between consumption expenditures and that level of income which could be achieved were all the factors employed.

So my best guess of what we might have here is a version of Friedman's "plucking model" (with full employment serving as a ceiling or capacity constraint) combined with some classical notion of the difficulty associated with matching the flow of national saving with the flow of national investment. This process evidently does not work well as it should unless the demand for investment is high--which, in turn, is not generally possible unless the economy (technology and/or population) is growing rapidly.

While the hypothesis seems similar to Keynes (1936) in that depressed investment is the proximate cause of persistently high unemployment, there is (I think) an important difference. Keynes emphasized the role of "animal spirits" in determining investment demand. Depressed expectations over the "prospective rate of profit on new investment" might become a self-fulfilling prophecy (see Farmer). Although I could be wrong, I don't ever recall Keynes suggesting that the cure for high unemployment was more rapid technological progress. I think of Keynes (1936) as an explanation for depressed levels, unrelated to growth phenomena.

Hansen, on the other hand, could be interpreted as holding the view that expectations are more firmly anchored on economic fundamentals ("...we are forced to regard the factors which underlie economic progress as the dominant determinants of investment and employment.") For this reason, Hansen seemed less enamored than Keynes on the use of expansionary fiscal policy to combat high unemployment. After all, if the fundamental problem is low growth, attempts to boost "aggregate demand" can at best confer only transitory benefits. Moreover, these benefits may over time be swamped by cost considerations, like a mounting public debt.

Insofar as Hansen (1939) provides policy advice, it sounds not so much like a pro-growth agenda as it does a set of anti-anti-growth recommendations. To paraphrase: "Population growth is fading. There are no new territories to settle and exploit. We can only hope for more technological advancement, so don't do anything to hamper this last great hope of ours. Except that it seems that we are: the growing power of trade unions, trade associations, and other monopolistic practices are restricting technological advance. This is a great folly."

Hansen's secular stagnation hypothesis was largely forgotten over time. I'm not entirely sure why this was the case, especially in light of the subsequent popularity of Keynesian theory. Maybe it had something to do with their respective policy recommendations. Active demand management sounds more appealing than dismantling trade unions, I suppose.

I sometimes hear people suggest that Hansen's hypothesis fell out of favor because it was proved wrong. Shortly after he wrote, the growth factors took off and the unemployment rate remained low on average. However, Hansen did not exactly offer a prognostication--his theory is better thought of (like any theory) as a conditional forecast.

While the settlement of new territory played a big role in the past, it was not likely to do so in the future (and in fact did not, as of 2016). And while medical technology played a big role in lowering mortality rates in the 19th and early 20th century, "no important further gains in this direction can possibly offset the prevailing low birth rate." To say that Hansen did not forecast the coming baby boom is correct only insofar as Hansen did not make any forecast--just a conditional statement that if the prevailing low birth rate was to persist into the future, then low population growth would contribute to depressed demand for capital formation. He was, of course, plainly concerned that the trend might continue, but that's not the same thing as asserting it would. His caution in making predictions is evident when he writes:

Of first-rate importance is the development of new industries. There is certainly no basis for the assumption that these are a thing of the past. But there is equally no basis for the assumption that we can take it for granted the rapid emergence of new industries rich in investment opportunities as the railroad, or more recently the automobile, together with all the related developments, including the construction of public roads to which it gave rise.

So maybe the pace of technological advance will accelerate. Or maybe it won't. It's not something we can take for granted. Hansen seems concerned about the prospect for future growth. But he's not asserting, as Robert Gordon seems to, that our best days are necessarily behind us. He notes, quite properly in my view, the sporadic nature of growth:

Nor is there any basis, either in history or theory, for the assumption that the rise of new industries proceeds inevitably at a uniform pace. The growth of modern industry has not come in terms of millions of small increments of change giving rise to smooth and even development. Characteristically, it has come by gigantic leaps and bounds.

He cites D. H. Roberston for this view, but it is also a recurring theme in Schumpeter's work (see my earlier post relating Schumpeterian growth to secular stagnation).

So, where does this leave us? No, I don't think Hansen's theory was proved wrong by subsequent developments. That the conditioning factors turned out not to prevail should not be construed as a rejection of the theory. The theory should be evaluated on other grounds.

The central proposition is that high growth (via technology and or population) is necessary to keep labor near "full employment" (the level of output near "potential.") In particular, high growth is necessary to stimulate the capital spending that will employ the labor input. I am curious to know what sort of empirical evidence one might bring to bear on this hypothesis. We have a lot more data at our disposal than Hansen. How should this data be organized? Should we estimate a Hamilton regime-switching model on growth rate regimes and correlate estimated growth regime against the average employment-to-population ratio? As well, there is the perennial question of how to identify theoretical objects like "full employment" or "potential GDP" in the data.

And even if we should find support for the hypothesis, there is the question of what sort of intervention, if any, might be desirable. On this issue, Hansen writes:

How far such a [stimulative] program, whether financed by taxation or borrowing, can be carried out without adversely affecting the system of free enterprise is a problem with which economists, I predict, will have to wrestle in the future far more intensely than in the past.

Well, he certainly got that prediction right!

How about measuring full employment as "every abled body that wants a job, has a job"? rather than rationalising full employment as some mythical figure that's never been measured properly (NAIRU) or claiming that those poor souls without a job are no unemployed since that can't exist, but are in fact enjoying leisure in place of work?

ReplyDeleteSure. But how does one measure "want a job" from available data? Even if we were to survey people, what would we ask? "Do you want a job?" Heck, yes. "How about cleaning toilets for minimum wage?" Um, no. So question is whether people want a good-paying job, commensurate with their skill (or one that even pays better than their skill). But how do we know what people view as "good paying jobs commensurate with their skills and work ethics?" It's a tricky business, if you think about it. I'm not saying it can't be done. It's just not something that is as obvious as people like to portray.

DeleteOh I agree it's a difficult subject! Only a fool would claim to have all the answers, probably because the said fool would not be blinkered by arguments on both sides of the debate?

DeleteFor example, why should unpleasant jobs (like cleaning toilets) offer only minimum wage? If there were adequate jobs in the market, then unpleasant and/or dangerous jobs would need to offer higher wages to attract applicants, or automate the process otherwise.

But then, that's the advantage (from my view) of having deliberate policy to maintain a percentage of the workforce unemployed, it means that those jobs that don't require skills but are unpopular can still be filled at the lowest possible cost, since someone will be desperate enough to take it out of necessity!

Why could the government not offer work for reasonable wages to any individual unable to find work in the private sector at a reasonable wage, since governments (federal/central at least) are not constrained by availability of currency - only real resources are it's limit! (if you want to ask who pays, recall Ben Burnanke's response to Scott Pelley about the Fed buying up assets during QE). Since we still have high unemployment (both here in the UK and in the States), a global surplus of building materials like steel and infrastructure that badly needs maintaining, elderly people badly needing care, and as you yourself once pointed out to Roger Farmer, wants not being met, there's plenty of scope for the Public sector to meet these demands, which might even encourage the Private sector to try and meet some of them too!

Heck, why not get the Government to fund proper, desirable skills training for the unemployed? After all, our government seems to be quite happy shovelling boatloads of cash to private companies in "make-work" training programmes of less use than a chocolate fireguard (see http://falseeconomy.org.uk/blog/esa-and-my-experience-of-skills-training-a4e-style as an example), why don't they use that cash to give proper training that yields good results?

Well, at least I can agree with your concluding paragraph.

DeleteI take it that means you don't agree with the other paragraphs. May I enquire why?

DeleteParagraph 1 I need no explanation - it's after all my opinion that only fools could form unbiased opinions, since all but the foolish can and are swayed by arguments from the same political and economic leaning of them. I'm unashamedly socialist (not in the Russia or North Korea sense, they are not examples of socialist economies, and only lazy capitalists evoke that argument in my opinion), so my beliefs and aspirations naturally lean towards more equitable distributions, rather than more efficient (which is typically less equitable).

Paragraph 2 - I suppose that the remuneration of unpleasant/dangerous jobs should be down to the employers of said jobs, but do you agree that such jobs are currently able to be filled at substandard wages because of the (relative) high unemployment experienced by most western economies is fair?

Paragraph 3 depends on if you believe in NAIRU and the Phillips curve. Personally I don't, and feel they are too easily used by governments to rationalise not taking policy choices to target real Full Employment (similar to what was experienced from the Post-war era to around the 1960s/70s.

I think I can understand why you cannot agree with paragraph 4 I think - it's pretty much the policy advocated by MMT, which I have found much to agree with, where the buffer stock represented by NAIRU presently is replaced with a buffer stock represented by a Job Guarantee, and requires subscription to the concept that the state, as the monopoly issuer of currency, can afford to pay for any goods, services and resources denominated in their issued currency, mindful only of inflationary risks as Full Employment is reached. But what parts of that do you actually disagree with, if you don't mind me asking?

Having never read Hansen, and frankly still at the beginning stages of my history of economic thought education, I can only ask a question: did Hansen give much weight to the legislative frictions put in place by the Roosevelt government?

ReplyDeleteProf J, I do not recall any mention of Roosevelt. Read the paper! I have a link to it above.

DeleteDavid,

ReplyDeleteHansen of course, wrote his paper while the world was still trying to pull itself out of the Great Depression, so there’s no surprise there’s an air of glumness about it.

It seems Alvin Hansen sat on the horns of a dilemma. He could see the stagnation of investment and the inability of capitalism to bring the required level of investment forth. On the other hand he was cautious about the desirability of government directed expenditure to fill the gap. And despite your explanations, it still seems strange, almost weird, that he doesn't mention Keynes in the paper given his views on the inadequacy of investment and the impotency of interest rates in moving investment are distinctly Keynesian notions. Sure these ideas aren't exclusively Keynesian but given he wrote the paper three years after the GT and that he even reviewed the GT (Oct 1936, Journal Of Political Economy) soon after it appeared seems odd. In the review, he was mildly disparaging of the GT and concluded that it did not form the basis for a "new economics" yet Hansen went on to develop the IS-LM analysis and penned the seminal "A Guide to Keynes". I imagine he could never quite fathom the degree of interest in the GT – Hansen’s ambivalence is puzzling. And of course Keynes never used the word technological in the GT and as you say he was pretty much only interested in finding a way out of the abyss the world economy had fallen into.

Was Hansen right to characterize the pattern of investment as secular? Secular suggests a very long term – perhaps 20 years. It would be difficult to say what Hansen described as secular as being secular. The 1910s and 1920s were a time when new technologies were bringing new products to market. The 1920s boom was a consumer and an investment boom. It came to an end for many reasons, one of them being that product saturation soon caught up with over investment. And there was the ensuing slump. So there was economic dislocation but it wasn’t secular and most of it was due to a saturated technology boom followed by a demand slump aggravated by perverse public policy. The shock of the slump, just as the slump of 2008/2009, required many years to dissipate.

So, I would argue that Hansen mischaracterized the stagnation as secular and failed to see that Keynesian prescriptions may have had more efficacy in pulling the world economy from its prolonged slump. A point I’m sure you will take issue with.

It could be argued that the Great Moderation of the 1980s and 1990s was the result of an investment boom in the new digital technologies of that era viz., personal computing, mobile communications, imaging and the internet. Again, saturation bringing about a collapse in investment and markets. It seems to me that the large part of the so called secular stagnation of the 2000s/2010s is due to similar factors described above and here we are again in an interregnum waiting for the next burst of commercialization of technological developments. It also seems to me it has been too easy for monetary theorists to blame this stagnation on perverse monetary policy and decision making. No doubt the next burst of growth and the next Great Moderation will be ascribed to the brand of monetary policy that is next captured by public fashion when in actuality it will be due to growth re-ignited by a new burst of technological innovation and commercialization.

These days the words secular stagnation and Japan seem to always go together. Monetarists see the Japanese malaise as the result of bad policy. In the 1980s, Japan was top of the economic heap. However, its internal cost structure eventually caught up with its success, leading to its demise. This was signalled by the collapse of the Tokyo property market in the late 1980s. Having become uncompetitive, the world looked to others, increasingly China, as a source of investment and cheap goods. Even the Japanese diverted domestic investment to China. This, I suggest, is more likely the cause of Japanese secular stagnation than spastic monetary policy.

Henry

Henry,

DeleteI have no idea what accounts for his apparent ambivalence toward Keynes. David Laidler suggests that he picked it up from the Swedes, who had developed many of Keynes' ideas before Keynes, and who thought that Keynes had not cited them properly.

Thanks for your comment!

I'm putting Laidler's book on the reading list. In a newspaper piece in 1928, written even before The Treatise on Money, Keynes made references to public spending as way out of the British 1920s slump, saying the suggestion was nothing new. I would imagine Keynes himself would say (and in fact he did say) the development of the GT was eclectic. Some people might say it is way off the mark, but you can see elements of Fisher's Theory of the Rate Interest in Keynes's liquidity preference theory.

DeleteHenry

"While the hypothesis seems similar to Keynes (1936) in that depressed investment is the proximate cause of persistently high unemployment, there is (I think) an important difference. Keynes emphasized the role of "animal spirits" in determining investment demand. Depressed expectations over the "prospective rate of profit on new investment" might become a self-fulfilling prophecy (see Farmer). Although I could be wrong, I don't ever recall Keynes suggesting that the cure for high unemployment was more rapid technological progress. I think of Keynes (1936) as an explanation for depressed levels, unrelated to growth phenomena."

ReplyDeleteKeynes did in fact produce his own version of a secular stagnation theory base on slowing population growth in an obscure article in the Eugenics Review (https://www.jstor.org/stable/1972863?seq=1#page_scan_tab_contents).

Here is a useful summaryof the article which also juxtaposes it to the General Theory (https://www.jstor.org/stable/2117053?seq=1#page_scan_tab_contents)

The entire SS idea strikes me as nonsense. The fact that little demand stems from investment / capital spending does not stop adequate demand coming from current spending. As to how to stimulate the latter demand, how about giving every household money to spend (and/or printing money and boost public spending)?

ReplyDeleteAs for Hansen's claim that there is some sort of clash between the latter form of stimulus and free enterprise, I don't get it. If households have more money to spend and they spend it on Ford cars, what is that a problem for the Ford Motor Company?