The Economy May Be Stuck in a Near-Zero World (Justin Wolfers).

Justin does a good job describing how many economists view the role of monetary and fiscal policy in the post Great Recession world of low interest rates and low inflation. I am curious to know where I agree and disagree with what he says. So, here goes.

[T]he real (inflation-adjusted) interest rate consistent with the economy operating at its full potential has fallen...from around 2.5 percent to 1 percent, or lower.

I think this is true. I also do not think it's surprising that the "natural rate of interest" (r*) fluctuates and that its trend path may shift over time. Indeed, I'd be surprised to learn this was not the case. According to standard macroeconomic theory, r* should follow the trend in consumption growth. The basic idea is simple. If the economy is expected to grow rapidly, people will want to save less (or borrow against their higher future income) in order to smooth their consumption. Collectively, their efforts to consume more and save less puts upward pressure on the real interest rate. The converse holds true if pessimism reigns: people will want to save more, to make provisions against a bleak future. Collectively, the effect is to depress the real interest rate.

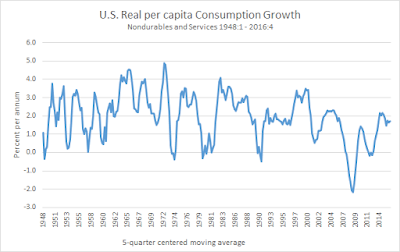

Of course, we cannot observe r*. But theory suggests it should be roughly proportional to consumption growth. We can observe consumption growth. Here is what the growth rate of real (inflation-adjusted) consumption of nondurables and services in the postwar U.S. looks like (series is smoothed):

If you're trained in the art of haruspicy, as most of us appear to be, then you'll divine all sorts of patterns from the picture above. You might see a 2 percent trend growth rate with a break down to 1 percent (or lower) in either 2000 or 2007. You might even detect a decade-long era of low growth in the 1970s.

Combined with the Fed's 2 percent inflation target, this implies...

In "normal times," the nominal interest rate -- the neutral interest rate plus inflation -- has fallen from around 6 percent to 3 percent. That creates a serious problem for the Fed. Here's why: Most recessions can be cured by lowering rates by several percentage points. When interest rates were closer to 6 percent, the Fed could lift the economy with plenty of leeway.

This is textbook stuff, which is not the same thing as saying it's correct. My own view on the matter (which is not necessarily correct either) is that the Fed is largely constrained to follow what the market "wants" in the way of real interest rates. It's not that the Fed "cures" a recession by lowering its policy rate -- the Fed is accommodating market forces that would have driven the real interest rate lower even in the absence of a central bank. Rightly or wrongly, the Fed acts to "smooth" these interest rate adjustments in the short-run. But at the end of the day, the trend path of r* is beyond the control of the Fed.

Yes, but what if r* is so low that the effective zero lower bound (ZLB) on the short-term nominal interest rate (the Fed's policy rate) prevents the Fed from accommodating what the market wants? With 2 percent inflation, the real interest rate can only decline to -2%. What if that's not low enough? Then something else has to give--for example, the unemployment rate will rise and remain elevated for as long as this unfortunate situation persists--a secular stagnation.

Perhaps the answer lies outside the Fed. It may be time to revive a more active role for fiscal policy--government spending and taxation--so that the government fills in for the missing stimulus when the Fed can't cut rates any further. Given political realities, this may be best achieved by building in stronger automatic stabilizers, mechanisms to increase spending in bad times, without requiring Congressional action.

In this spirit, Justin recommends a mechanism that automatically increases funding for infrastructure programs when economic growth slows. I personally don't think this is a terrible idea. (Though, I'd rather that infrastructure be geared more to long-term needs.) But no doubt it's probably easier said than done.

Sometimes though, when I sit back and reflect on this line of thinking, it strikes me as rather odd in a couple of respects.

First, is the ZLB really a significant economic problem? If it is, then why not abolish it as recommended by Miles Kimball? Would permitting significantly negative real rates of interest solve our problems? I don't think so. I'm inclined to think of a low r* as symptomatic of more fundamental economic forces. And eliminating any (real or perceived) gap between the market interest rate and r* is probably small potatoes (see here).

If r* is low, then we need to ask why it is low. There's no shortage of possible explanations out there (low productivity growth, demographics, etc.). If we somehow decide we'd like to see it higher, the solution is likely to be found in growth-promoting policies. (Whether we want growth-promoting policies is a completely separate matter, by the way. Personally, I think more attention should be paid to policies that encourage social cohesion, which may or may not be consistent with higher growth. But this is a column for another day.)

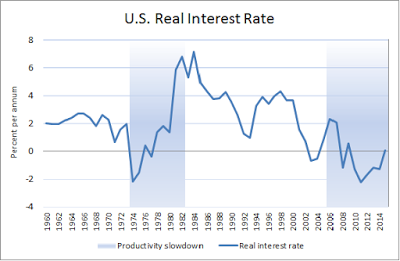

Second, I think the world has indeed changed for discretionary monetary and fiscal policy, but in a way that almost no one talks about. Quite apart from any possible changes in r* (which we cannot measure), the real rate of return on U.S. Treasury (UST) debt--what my boss James Bullard calls "r-dagger"--has been declining for over 30 years (diagram taken from here).

One interpretation of this pattern is that USTs were initially a flight-to-safety vehicle with the disruptions that occurred in the early 1970s (so real yields declined). With the breakdown of Bretton Woods and fiscal pressures (Vietnam war, War on Poverty, etc.), however, inflation became un-anchored. The high real yield on nominal UST debt reflected a growing inflation-risk premium in the early 1980s (when inflation was high and volatile). Subsequently, as inflation declined and inflation expectations became anchored (thanks to Volcker and a terrible recession) the inflation risk premium declined over time. Since about 2000, a China trade shock and other factors led to a growing world demand for USDs and USTs. R-dagger (r+) remains extremely low even today--reflecting the "liquidity premium" that the market now attaches to UST debt.

Moreover, the distinction between USDs and USTs is much diminished in financial markets. In the old days, when the Fed wanted to move interest rates through an open-market swap of USD for UST, it meant something. But today, it means almost nothing, since interest-bearing reserves are a very close substitute for interest-bearing treasuries. In short, U.S. treasury debt is essentially "money" as far as financial markets are concerned (USTs circulate as such in repo markets, for example).

The implication of all this for monetary and fiscal policy is quite interesting. The fact that the yield on USTs is less than (our estimate of) the natural rate of interest suggests that the policy rate is presently too low -- not too high (as is suggested by standard ZLB concerns). The most direct way to raise interest rates (i.e., eliminate the liquidity premium on USTs) is for the U.S. treasury to issue debt at a faster pace. One way to do this is through Justin's automatic infrastructure funding plan that kicks in when liquidity premia on USTs are elevated (bond yields are low). Another way is to have automatic (temporary) tax cuts kick in. Yet another way (though far less desirable) is to have the Fed increase the interest in pays on reserves. Politically this is dynamite, but from an economic perspective, it forces (ceteris paribus) the treasury to issue debt at a faster pace (because it lowers Fed remittances to the treasury). Yet another way is to have the Fed sell some of its treasury holdings (since treasuries are sometimes more liquid than reserves in financial markets--i.e., only depository institutions have direct access to reserves).

Depending on which view one adopts, the recommended Fed policy action matters a great deal (at least, in principle, if not quantitatively). If the interest rate is too high (ZLB view), then it should be lowered, or the inflation target raised. If the interest rate is too low (liquidity premium view), then it should be raised, through asset sales or some other mechanism.

On the other hand, the recommended Treasury policy action seems robust across the two views: the treasury should expand its debt at a faster pace (via tax cuts or increased spending, or some combination). This seems like a promising development from the perspective of competing theories. If a policy recommendation follows from many different perspectives, we become more comfortable with the idea of actually implement them. Of course, there are some caveats to consider, which I discuss here. But enough for today.

Justin does a good job describing how many economists view the role of monetary and fiscal policy in the post Great Recession world of low interest rates and low inflation. I am curious to know where I agree and disagree with what he says. So, here goes.

[T]he real (inflation-adjusted) interest rate consistent with the economy operating at its full potential has fallen...from around 2.5 percent to 1 percent, or lower.

I think this is true. I also do not think it's surprising that the "natural rate of interest" (r*) fluctuates and that its trend path may shift over time. Indeed, I'd be surprised to learn this was not the case. According to standard macroeconomic theory, r* should follow the trend in consumption growth. The basic idea is simple. If the economy is expected to grow rapidly, people will want to save less (or borrow against their higher future income) in order to smooth their consumption. Collectively, their efforts to consume more and save less puts upward pressure on the real interest rate. The converse holds true if pessimism reigns: people will want to save more, to make provisions against a bleak future. Collectively, the effect is to depress the real interest rate.

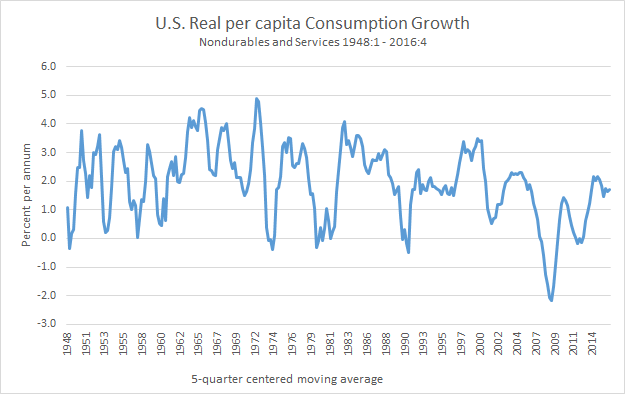

Of course, we cannot observe r*. But theory suggests it should be roughly proportional to consumption growth. We can observe consumption growth. Here is what the growth rate of real (inflation-adjusted) consumption of nondurables and services in the postwar U.S. looks like (series is smoothed):

If you're trained in the art of haruspicy, as most of us appear to be, then you'll divine all sorts of patterns from the picture above. You might see a 2 percent trend growth rate with a break down to 1 percent (or lower) in either 2000 or 2007. You might even detect a decade-long era of low growth in the 1970s.

Combined with the Fed's 2 percent inflation target, this implies...

In "normal times," the nominal interest rate -- the neutral interest rate plus inflation -- has fallen from around 6 percent to 3 percent. That creates a serious problem for the Fed. Here's why: Most recessions can be cured by lowering rates by several percentage points. When interest rates were closer to 6 percent, the Fed could lift the economy with plenty of leeway.

This is textbook stuff, which is not the same thing as saying it's correct. My own view on the matter (which is not necessarily correct either) is that the Fed is largely constrained to follow what the market "wants" in the way of real interest rates. It's not that the Fed "cures" a recession by lowering its policy rate -- the Fed is accommodating market forces that would have driven the real interest rate lower even in the absence of a central bank. Rightly or wrongly, the Fed acts to "smooth" these interest rate adjustments in the short-run. But at the end of the day, the trend path of r* is beyond the control of the Fed.

Yes, but what if r* is so low that the effective zero lower bound (ZLB) on the short-term nominal interest rate (the Fed's policy rate) prevents the Fed from accommodating what the market wants? With 2 percent inflation, the real interest rate can only decline to -2%. What if that's not low enough? Then something else has to give--for example, the unemployment rate will rise and remain elevated for as long as this unfortunate situation persists--a secular stagnation.

Perhaps the answer lies outside the Fed. It may be time to revive a more active role for fiscal policy--government spending and taxation--so that the government fills in for the missing stimulus when the Fed can't cut rates any further. Given political realities, this may be best achieved by building in stronger automatic stabilizers, mechanisms to increase spending in bad times, without requiring Congressional action.

In this spirit, Justin recommends a mechanism that automatically increases funding for infrastructure programs when economic growth slows. I personally don't think this is a terrible idea. (Though, I'd rather that infrastructure be geared more to long-term needs.) But no doubt it's probably easier said than done.

Sometimes though, when I sit back and reflect on this line of thinking, it strikes me as rather odd in a couple of respects.

First, is the ZLB really a significant economic problem? If it is, then why not abolish it as recommended by Miles Kimball? Would permitting significantly negative real rates of interest solve our problems? I don't think so. I'm inclined to think of a low r* as symptomatic of more fundamental economic forces. And eliminating any (real or perceived) gap between the market interest rate and r* is probably small potatoes (see here).

If r* is low, then we need to ask why it is low. There's no shortage of possible explanations out there (low productivity growth, demographics, etc.). If we somehow decide we'd like to see it higher, the solution is likely to be found in growth-promoting policies. (Whether we want growth-promoting policies is a completely separate matter, by the way. Personally, I think more attention should be paid to policies that encourage social cohesion, which may or may not be consistent with higher growth. But this is a column for another day.)

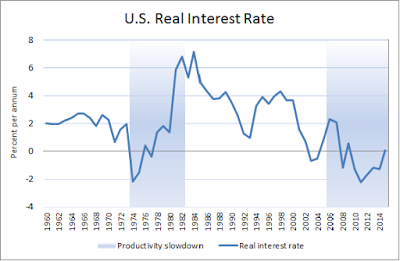

Second, I think the world has indeed changed for discretionary monetary and fiscal policy, but in a way that almost no one talks about. Quite apart from any possible changes in r* (which we cannot measure), the real rate of return on U.S. Treasury (UST) debt--what my boss James Bullard calls "r-dagger"--has been declining for over 30 years (diagram taken from here).

One interpretation of this pattern is that USTs were initially a flight-to-safety vehicle with the disruptions that occurred in the early 1970s (so real yields declined). With the breakdown of Bretton Woods and fiscal pressures (Vietnam war, War on Poverty, etc.), however, inflation became un-anchored. The high real yield on nominal UST debt reflected a growing inflation-risk premium in the early 1980s (when inflation was high and volatile). Subsequently, as inflation declined and inflation expectations became anchored (thanks to Volcker and a terrible recession) the inflation risk premium declined over time. Since about 2000, a China trade shock and other factors led to a growing world demand for USDs and USTs. R-dagger (r+) remains extremely low even today--reflecting the "liquidity premium" that the market now attaches to UST debt.

Moreover, the distinction between USDs and USTs is much diminished in financial markets. In the old days, when the Fed wanted to move interest rates through an open-market swap of USD for UST, it meant something. But today, it means almost nothing, since interest-bearing reserves are a very close substitute for interest-bearing treasuries. In short, U.S. treasury debt is essentially "money" as far as financial markets are concerned (USTs circulate as such in repo markets, for example).

The implication of all this for monetary and fiscal policy is quite interesting. The fact that the yield on USTs is less than (our estimate of) the natural rate of interest suggests that the policy rate is presently too low -- not too high (as is suggested by standard ZLB concerns). The most direct way to raise interest rates (i.e., eliminate the liquidity premium on USTs) is for the U.S. treasury to issue debt at a faster pace. One way to do this is through Justin's automatic infrastructure funding plan that kicks in when liquidity premia on USTs are elevated (bond yields are low). Another way is to have automatic (temporary) tax cuts kick in. Yet another way (though far less desirable) is to have the Fed increase the interest in pays on reserves. Politically this is dynamite, but from an economic perspective, it forces (ceteris paribus) the treasury to issue debt at a faster pace (because it lowers Fed remittances to the treasury). Yet another way is to have the Fed sell some of its treasury holdings (since treasuries are sometimes more liquid than reserves in financial markets--i.e., only depository institutions have direct access to reserves).

Depending on which view one adopts, the recommended Fed policy action matters a great deal (at least, in principle, if not quantitatively). If the interest rate is too high (ZLB view), then it should be lowered, or the inflation target raised. If the interest rate is too low (liquidity premium view), then it should be raised, through asset sales or some other mechanism.

On the other hand, the recommended Treasury policy action seems robust across the two views: the treasury should expand its debt at a faster pace (via tax cuts or increased spending, or some combination). This seems like a promising development from the perspective of competing theories. If a policy recommendation follows from many different perspectives, we become more comfortable with the idea of actually implement them. Of course, there are some caveats to consider, which I discuss here. But enough for today.

The whole r* concept is nonsense. Reason is that the rate of interest compatible with full employment is dependent on the size of the national debt, and the latter can be altered / manipulated at will by the government and central bank of a country that issues its own money.

ReplyDeleteE.g. if a government brought about an irresponsibly high amount of debt, the private sector would not be willing to hold that other than at an elevated rate of interest. Or governments are free to go the other way, and have a relatively low amount of national debt and low interest rates.

Hi Ralph, the notion of an interest rate being related to a level object (like output or employment) is somewhat subtle. As Nick Rowe likes to point out once in a while, the real interest rate reflects more the *change* in consumption (or output), not the level. I discuss the issue a bit here: http://andolfatto.blogspot.com/2016/04/interest-rates-and-aggregate-demand.html

DeleteI just wonder why and how the Fed is "constrained" by a ZLB when it has the option of temporarily raising the rate of inflation (using QE) and it necessary the long run inflation target.

ReplyDeleteYou are correct, in principle. But in practice, Fed it is difficult. See: http://andolfatto.blogspot.com/2015/05/understanding-lowflation.html

DeleteBottom line; optimal policy choices are consistently sabotaged by a) faith-based ideology over fact-based reality, and b)regulatory capture.

ReplyDeleteGood article! I found several related articles -- and found them all interesting -- after reading yours.

ReplyDeleteYou write: "If r* is low, then we need to ask why it is low." This question would seem to demand more attention and better answers, if the importance of r* is as great you describe.