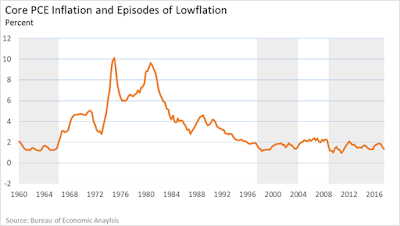

The term "lowflation" was initially coined by economists at the IMF in 2014 (see here). It refers to an inflation rate that is persistently low (relative to some target) and positive (so, not deflation). Here is what lowflation looks like in the United States:

How should we think about lowflation? I've written a bit on the subject here and here. Is the phenomenon unusual? Is it something we should worry about?

As it turns out, the phenomenon is not unusual even in recent U.S. monetary history. The following diagram plots the PCE core inflation rate for the United States since 1960. The shaded areas represent "lowflation" episodes--periods in which PCE core inflation is below 2%.

The early 1960s was also an era of lowflation. So was the more recent period 1996-2003. The period 2004-2008 of (slightly above 2%) inflation seems more like a recent aberration.

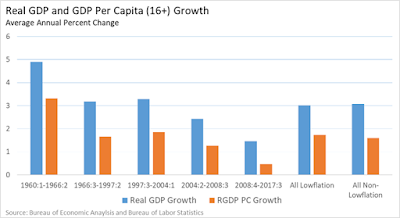

Is lowflation a problem? Perhaps. But if it is, it certainly doesn't seem to show up in the economy's RGDP growth performance. The following figure plots the growth rate of RGDP and RGDP per capita for each of the high and low inflation episodes identified in the early figure.

In this sample period, economic growth in lowflation episodes averages about the same as growth in non-lowflation episodes. What is one to make of this?

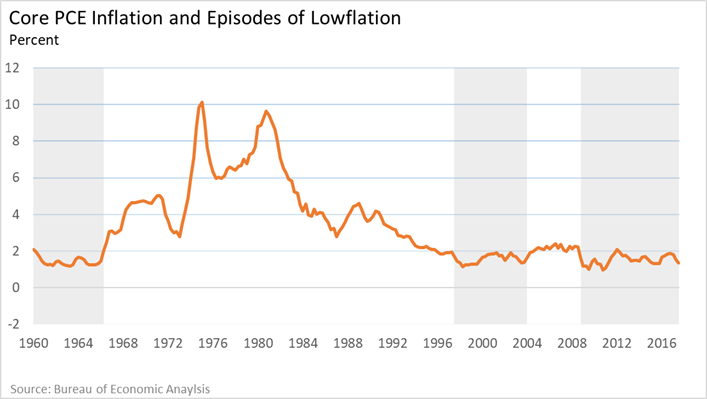

As it turns out, the phenomenon is not unusual even in recent U.S. monetary history. The following diagram plots the PCE core inflation rate for the United States since 1960. The shaded areas represent "lowflation" episodes--periods in which PCE core inflation is below 2%.

The early 1960s was also an era of lowflation. So was the more recent period 1996-2003. The period 2004-2008 of (slightly above 2%) inflation seems more like a recent aberration.

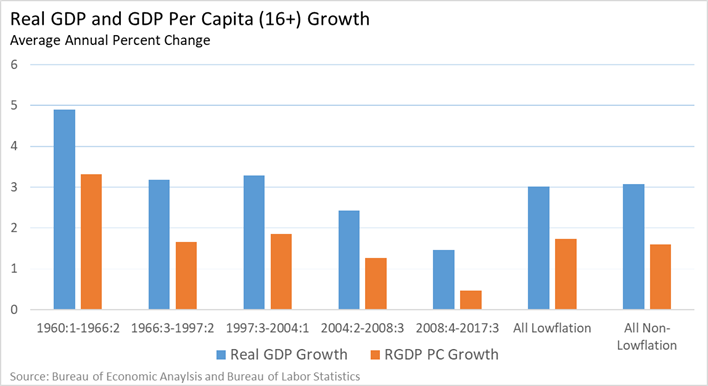

Is lowflation a problem? Perhaps. But if it is, it certainly doesn't seem to show up in the economy's RGDP growth performance. The following figure plots the growth rate of RGDP and RGDP per capita for each of the high and low inflation episodes identified in the early figure.

That money is neutral in the long run?

ReplyDeleteNot necessarily. Inflation can still (in theory, at least) affect the *level* of RGDP without affecting its long-run growth rate. (In this case we would say that money is not superneutral.)

DeleteFair enough. But what is the magnitude of that effect in the case of the US? Inflation never reached the levels that severely disrupted economic activity (aside from the painful disinflation that ended it).

DeleteThat lowflation is largely caused by positive supply shocks? And that it fortunately hasn't yet caused a de-anchoring of long-run inflation expectations from the target (which probably would be a problem)?

ReplyDeletemoney is not what puts pressure on prices, demand is

ReplyDeletedemand is income not money

income is money times the velocity of money,